Tamamlanan Tüm Projeleri Görmek İçin Tıklayınız

Altyapı Varlık Sınıfı

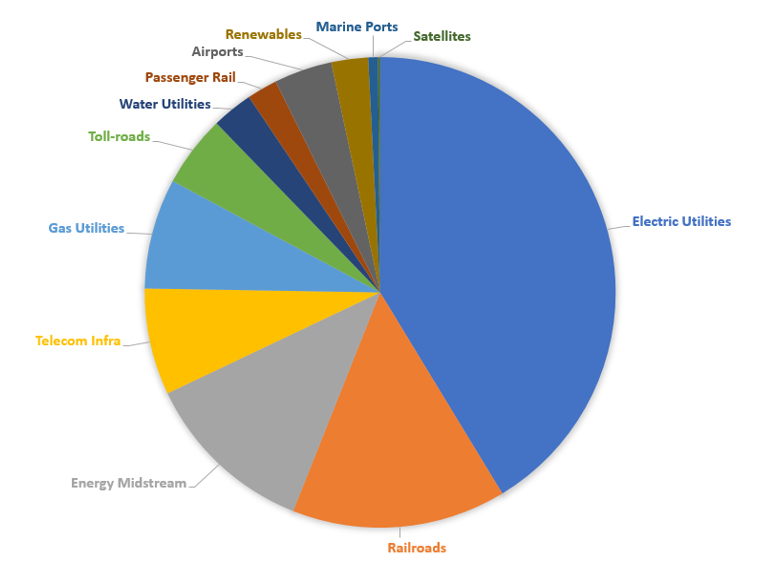

Pek çok varlık dağılımı modeli, “gerçek varlıklar”a, yani altyapı ve gayrimenkule yaklaşık %10 ağırlık verilmesini önerir. Altyapı, enerji santralleri, demir yolları, enerji ara hat boru hatları, veri merkezleri ve telekom ağlarını içerir. Ayrıca doğalgaz hizmetleri, ücretli yollar, havaalanları, deniz limanları ve uydulara da yatırım yapma imkânı sunar.

Kaynak: Küresel Listeleme Altyapı Organizasyonu (GLIO)

Altyapı varlık sınıfının sıklıkla bahsedilen bir avantajı, daha istikrarlı, sözleşmeyle desteklenen uzun vadeli nakit akışlarıdır—bu da desteklenen getirilerin şu anda %4,5 civarında olmasını sağlar. Nakit akışları genellikle yükselen varlık değerleri ile enflasyona karşı sözleşmeyle korunur ve bu da bir değer koruma mekanizması olabilir. Portföydeki varlıklar için bir diğer istatistiksel avantaj ise, düşük beta ve diğer varlıklar ve sektörlerle düşük korelasyonlu bir varlık sınıfının eklenmesiyle sağlanan çeşitlendirme faydalarıdır. Diğer yandan, altyapı hisseleri için potansiyel olumsuzlar, gelişen piyasa etkileri, sözleşme ödüllerinin düzensizliği ve yükselen piyasada algılanan büyüme sınırları nedeniyle daha kısa vadeli volatilite olabilir. Son üç yıl içinde, diğer küresel endekslerle kıyaslandığında, uzun vadeli nakit akışları üzerinde yükselen faiz oranlarının büyük etkisi önemli bir engel olmuştur. Bu nedenle, faiz oranı tartışmaları—faiz oranlarının daha da yükselmesi, yakında düşmesi veya uzun vadede daha yüksek olması—bu alanı etkileyebilir. Faiz oranları bir kenara bırakıldığında, önümüzdeki yıllarda altyapı büyümesi için birçok potansiyel itici güç bulunmaktadır. Bunlardan biri, Rusya’nın Ukrayna’daki savaşı ile hızla ön plana çıkan net bir itici güçtür: Malzeme ve üretim endüstrilerinin yeniden yerleştirilmesi yoluyla küreselleşmeden uzaklaşma eğilimi. Deniz limanı varlıkları etkilenebilir ve CHIPS Yasası gibi politikaların ardından yatırım harcamaları ve ilişkili nakit akışlarının gerçekleşmesi zaman alabilir. Ancak, büyüyen sanayi tabanlarını desteklemek ve iç pazarda tedarik zincirlerini yeniden düzenleyerek engelleri kaldırmak için önemli yeni altyapılar gerekecektir. Altyapı büyümesini destekleyen bir diğer önemli etken, ekonomiyi karbon salınımından arındırmak için önümüzdeki yıllarda yapılacak birçok iş olacaktır. Birçok uzman, sıcaklık değişimini sınırlamak için yılda 1.5-2 trilyon dolar arasında harcama yapılması gerektiğini, bu miktarın bugünkü harcamaların birkaç katı olduğunu belirtmektedir. Küresel politika adımları hız kazanıyor. Örneğin, Enflasyon Azaltma Yasası büyük altyapı bileşenlerine sahip ve zorunlu emisyon raporlama, düşük karbonlu altyapı yatırımlarını teşvik edebilir. Daha düşük karbonlu bir dünyada elektrifikasyon bir zorunluluk haline geldiğinden, ek yükleri ve yeni yükleri taşıyabilmek için hem ana iletim hatlarında hem de yerel dağıtımda önemli altyapılar gereklidir. Özellikle yerel düzeyde, fırtınalardan sistemleri korumak, gelişen elektrikli araç (EV) şarj yüklerini karşılayacak kapasite eklemek, enerji verimliliği çabalarını desteklemek ve sürekli artan dijitalleşme taleplerini karşılamak için çok daha fazla kamu hizmeti çalışması yapılmaktadır. Genel olarak enerji sektörü, yenilenebilir enerji üretim kapasitesi ve batarya sistemleri eklemek konusunda oldukça aktiftir. Bunların hepsi şebeke üzerinde etkiler yaratır ve yenilenebilir enerji kapasitesinin ne zaman ve nerede eklenmesine izin verileceği senaryolarına dayalı olarak bazı planlama zorlukları oluşturabilir. Doğalgaz, küresel enerji ihtiyacındaki büyümeye katkıda bulunurken, kömür, odun ve yakılmış biyokütle gibi yüksek karbon emisyonuna sahip enerji kaynaklarına kıyasla daha düşük karbon emisyonu sunan bir alternatif olarak rol oynayacaktır. Hidrojen ve karbondioksit boru hatları da bir fırsat oluşturmalıdır. LNG sıvılaştırma ve gazlaştırma tesisleri ile bunlara hizmet veren boru hatlarının eklenmeye devam etmesi gerekmektedir, çünkü ithal edilen gaz, birçok ülkenin emisyonları yönetmesine yardımcı olacak (daha az kömür kullanımı). Doğalgaz hizmetlerinde, bazı bölgelerde yeni doğalgaz bağlantılarına yönelik kısıtlamalar, teslimat büyümesini zorlayabilir, ancak düzenlemelerle yapılan harcamaların, sızıntıları azaltmak, dayanıklılığı artırmak, daha düşük maliyetli izleme sistemleri eklemek ve mümkün olduğunda verimliliği iyileştirmek için teşvik edilmesi gerekir. Karbon emisyonu açısından en düşük yoğunluğa sahip ulaşım yöntemlerinden biri olarak demiryolları, tüm tedarik zincirlerinde karbon emisyonlarının artan maliyet algısından fayda sağlamaya devam etmektedir. Deniz limanları, küresel ticaretten uzaklaşma nedeniyle olumsuz etkilenebilir, ancak limanlar aynı zamanda daha düşük karbon ayak izleri ve kara içi dağıtım merkezleriyle daha güçlü lojistik bağlantılar kurmak için harcama yapacaklardır. Ücretli yollar için, genellikle benzinli araçlardan daha ağır olan ve yolları daha fazla aşındıran elektrikli araçlara (EV’ler) yönelik kademeli geçiş, yol bakımına ek baskı yapmaktadır ve sürücüler için birden fazla yakıt seçeneğini karşılayacak altyapı harcamalarını gerektirmektedir (benzin, dizel, elektrik, hidrojen). Benzinli araç sayısının azalmasıyla benzin vergileri düştükçe, birçok bölge, vergi uygulamak için galon başına değil, mil başına veya yol ücreti (toll) bazında bir sistem benimsemeyi gerekli bulabilir. Ve aslında, profesyonel ücretli yol işletmecileriyle sözleşme yapmanın daha hızlı bir seçenek olabileceğini görebilirler. Altyapı varlıkları uzun ömürlü olup, hizmete alınmaları yıllar sürebilir, bu nedenle bir şeyin aniden daha hızlı veya daha derinlemesine bilinmesi, varlık profillerinde, kapasitede veya nakit akışlarında anında değişim anlamına gelmez. Bunun yerine, makine öğrenimi ve tesis optimizasyonu ile geçmişte yapılan endüstri çabaları, yapay zeka ve daha fazla veri setinin uygulanmasıyla daha da güçlü hale gelmelidir. Yapay zeka (AI) hesaplama ihtiyaçları, önemli miktarda elektrik gereksinimi doğurur, ancak kamu hizmetleri de AI’yi daha ayrıntılı yerel kullanım analizleri yapmak, mahalle bazında kesinti tahminleri oluşturmak, öngörücü hizmet gereksinimlerini belirlemek, daha hızlı hizmet yanıt süreleri sağlamak ve değişen elektrikli araç (EV) şarj taleplerini yönetmek için kullanabilir. Rüzgar, güneş ışığı seviyeleri ve yağış miktarı gibi verilerin makine öğrenimi analizine dahil edilmesi, son kilometre hizmetlerini daha da optimize etmeye yardımcı olmalıdır. Doğalgaz boru hatları ve dağıtım sistemleri için, karbon emisyonlarını ve metan sızıntılarını izlemek, hava koşullarını dahil etmek gibi unsurlar, boru hatları ve dağıtım sistemlerinin AI kullanarak iyileştirebileceği alanlardır. Demiryolları yıllardır lojistik, sensörler, vagon yönetimi ve demiryolu vagonu konumları gibi alanlarda operasyonlarını optimize etmek için çeşitli veri zekasından faydalanmaktadır. YZ’nin, yakıt tüketimini etkileyen demiryolu eğimleri gibi faktörleri dikkate alarak kullanılmaya devam edilmesi, tren uzunlukları ve güzergahlarının optimize edilmesinde göz önünde bulundurulabilecek daha yeni bir ilgi alanının örneğidir. Yolculuklarda, yol projelerinde eğimleri dikkate almanın yanı sıra, yapay zeka (YZ) değişen trafik akışlarını yönlendirmek, farklı araç türlerini (otonom araçlar dahil) accommodate etmek, kamu güvenliğini artırmak ve trafik seviyeleri arttıkça veya en azından Covid öncesi normlara döndükçe talep fiyatlandırmasını optimize etmek için kullanılabilir. Veri merkezleri ve telekom ağı altyapıları, yapay zeka kullanımındaki büyüme ve artan iletim hızlarından faydalanmaya devam etmelidir. Bu, kullanıcılara daha yakın sistemleri (yani, daha küçük kuleler ve kulelerle birlikte yerleştirilen veri merkezleri) tercih eden bir eğilim yaratmaktadır. Dijitalleşme ve dijital para birimlerini ve yapay zekayı desteklemek için artan enerji talebi, daha fazla veri merkezi ve daha hızlı ağlar (kablolu, kablosuz ve uydu) ihtiyacını sürdürmeye devam etmektedir. Önümüzdeki dönemdeki ticaret akışlarının yeniden değerlendirilmesi, karbon salınımından arındırma ve yapay zeka gibi değişiklikler, altyapı varlık sınıfının gelecekteki büyümesine ve operasyonların iyileştirilmesine yardımcı olmalıdır. Gelecekte birçok proje harcama fırsatı olacaktır. Bu uzun vadeli büyüme, ekonominin yavaşlaması durumunda bile varlık sınıfını desteklemeye yardımcı olmalıdır—özellikle faiz oranları, uzun vadeli nakit akışı üreten varlıklara yeniden destek olursa.Son Performans

Önümüzdeki Altyapı Fırsatları

Güç

Enerji Ara Hattı

Ulaşım

Yapay Zeka ve Altyapı

Güç

Ulaşım

Telekom Altyapı İnşaatı

Sonuç

Sektörler